Broadcom’s report details its dual‐core strategy, merging semiconductors with infrastructure software. It covers company overview, key M&A including the VMware deal, and revenue breakdown (FY2024: $51.6B; FY2025: ~$60B). Margin gains to ~70% and recurring revenue drive growth despite integration and cyclicality risks. Margins and software growth boost firm value! The 1‑year target price is $220.

Table of Content

Executive Summary

Company Overview

Historical Overview – Mergers & Acquisitions

-Timeline – VMware Ownership & Acquisition History

-VMware’s Financial Contribution – Before vs. After Acquisition

-GAAP vs. Non-GAAP Financial Metrics – FY2024

-Other Recent Mergers and Acquisitions

Revenue Breakdown

Business Segment Analysis

-Semiconductor Solutions

-Infrastructure Software

Market Position and Strategic Insights

-Semiconductors (Competitive Positioning)

-Semiconductors (Market Trends & Growth)

-Infrastructure Software

-Strategic Outlook

-Future Growth Potential

-Conclusion

Key Developments (2020–2025)

-2020

-2021

-2022

-2023

-2024

-2025

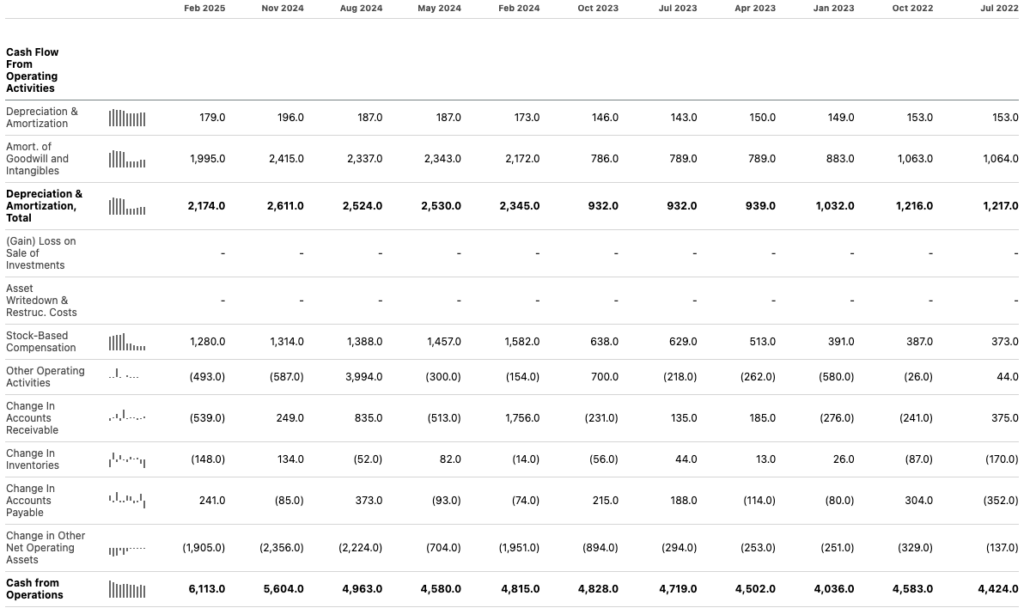

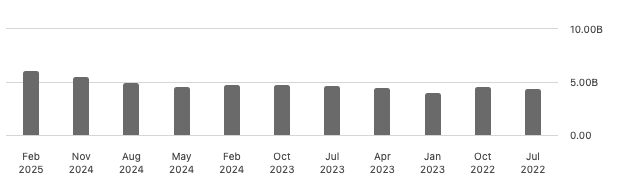

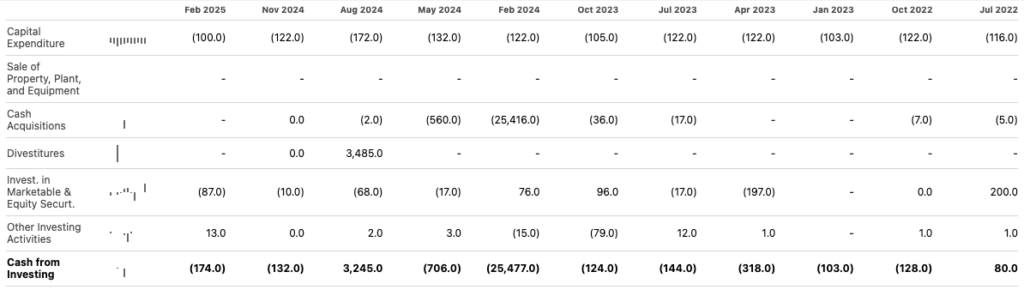

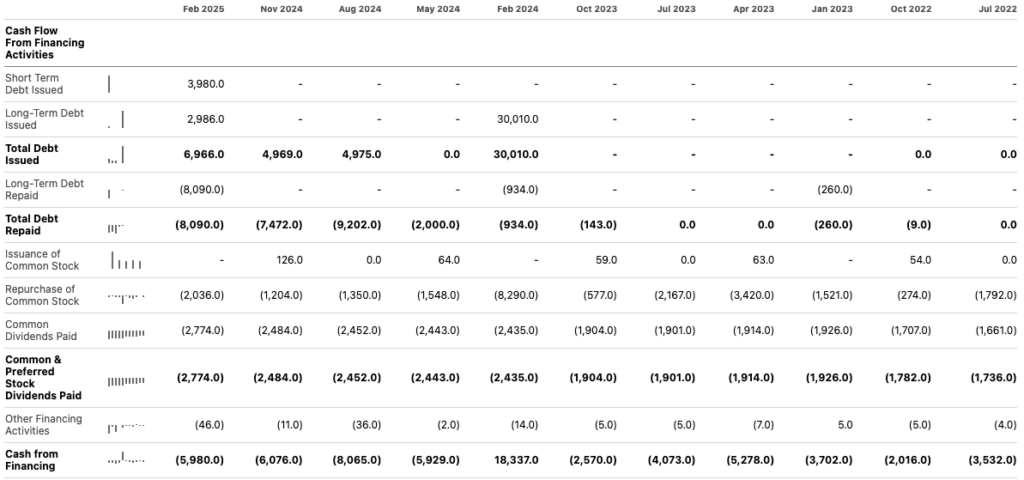

Financial Statement Analysis

-Income Statement

-Balance Sheet

-Cash Flow Statement

Valuation

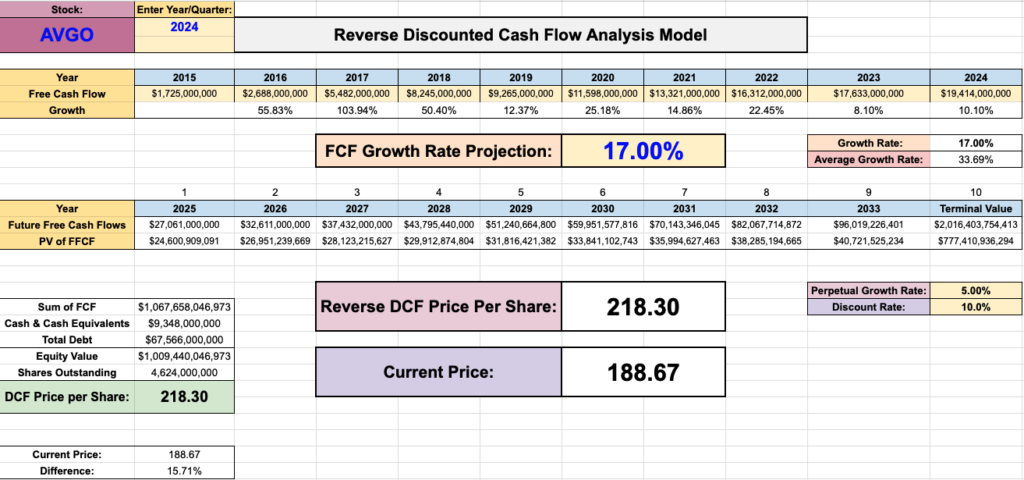

-Discounted Cash Flow (DCF) Analysis

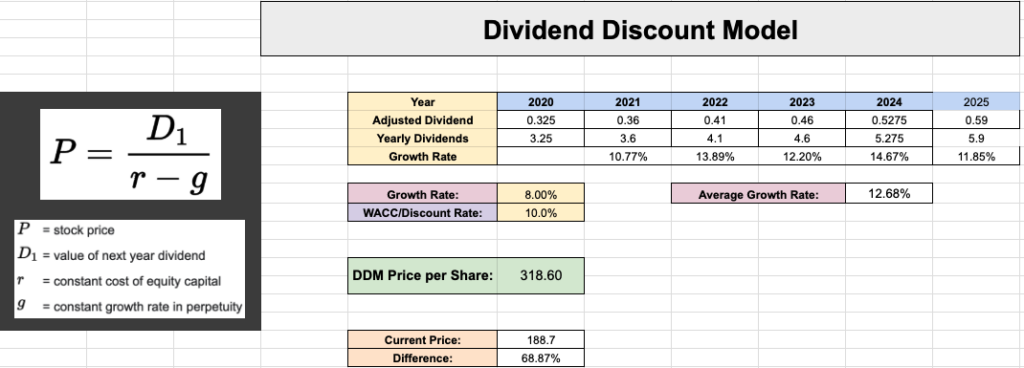

-Dividend Discount Model (DDM)

-Other Valuation Methods and Signals

-Overall Price Target and Conclusion

Investment Opportunities and Risks

-Investment Opportunities

-Investment Risks

Executive Summary

This report delivers a comprehensive analysis of Broadcom Inc., emphasizing its dual-core business model that merges semiconductor solutions with an expanding infrastructure software division. The report is organized into several sections: a company overview, a historical review of key mergers and acquisitions—including the transformative VMware deal—a detailed revenue breakdown by business segment, and an assessment of investment opportunities and risks.

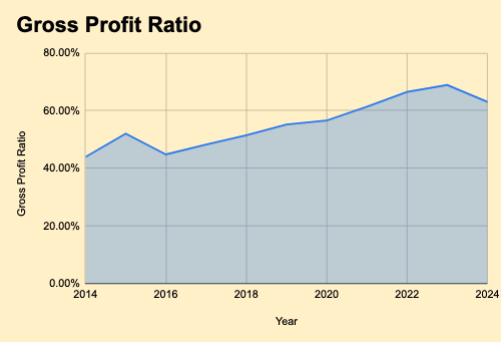

Key findings highlight Broadcom’s strategic transformation. Historically recognized as a semiconductor leader, Broadcom has diversified its revenue streams by integrating software through significant acquisitions. With a current stock price of approximately $195 per share and a market capitalization nearing $920 billion, the integration of VMware has boosted infrastructure software revenue to account for roughly one-quarter of total sales. Moreover, operating margins have surged from about 30% pre-acquisition to an impressive 70% post-integration, reflecting substantial efficiency improvements.

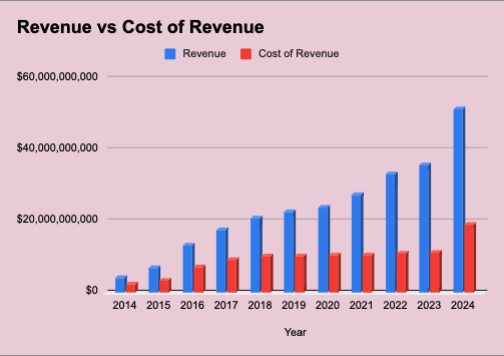

Critical data include FY2024 total revenues of $51.6 billion, comprising $30.1 billion from Semiconductor Solutions and nearly $21.5 billion from Infrastructure Software. Projections indicate that FY2025 revenues may reach around $60 billion, driven by robust demand for AI-related chips and a strategic shift toward recurring subscription-based software revenue.

Based on these insights, a one-year target price of $220 has been established. This valuation reflects Broadcom’s strong growth prospects, underpinned by its diversified portfolio and operational enhancements. Key investment opportunities lie in the company’s ability to innovate and capture market share in high-growth segments, while risks include integration challenges, cyclical semiconductor demand, and intensified competition from peers.

Company Overview

Broadcom Inc. (NASDAQ: AVGO) is a leading global technology company that designs, develops, and supplies a broad range of semiconductor and enterprise software products. In the semiconductor domain, Broadcom’s portfolio includes networking and data center chips, broadband and wireless connectivity solutions (Wi-Fi/Bluetooth), storage and mainframe processors, and other integrated circuits. On the software side, Broadcom provides infrastructure and security solutions, including mainframe software (from CA Technologies), enterprise security (from Symantec), and virtualization/cloud software (from VMware). This dual-core business model positions Broadcom in both the semiconductor industry and the enterprise infrastructure software industry.

Broadcom’s stock is listed on NASDAQ under the symbol AVGO. As of mid-March 2025, the stock trades around $195 per share, giving Broadcom a market capitalization near $920 billion. The trailing price-to-earnings (P/E) ratio is exceptionally high – roughly 90 based on GAAP earnings. This elevated P/E reflects recently depressed GAAP net income following a major acquisition (VMware). Broadcom’s dividend is $0.59 per quarter (post-2024 split), continuing a long trend of annual dividend increases. Overall, Broadcom has achieved significant scale through both organic innovation and strategic acquisitions, becoming one of the world’s largest semiconductor and infrastructure software companies. In the following sections, we examine Broadcom’s key historical mergers – most notably VMware – and their impact on the company’s financial performance.

Historical Overview – Mergers & Acquisitions

Timeline – VMware Ownership & Acquisition History

- 1998: VMware is founded as a pioneer in x86 server virtualization.

- 2004: EMC Corporation acquires VMware for about $625 million, making VMware a subsidiary of EMC.

- August 2007: EMC conducts an IPO for ~10% of VMware’s shares, raising ~$957 million (VMware stock nearly doubled on first day). EMC retains an ~90% ownership stake.

- 2016: Dell Technologies acquires EMC (including EMC’s VMware stake) in a $67 billion deal. VMware becomes majority-owned by Dell but remains an independent publicly traded company (Dell controlling ~81%).

- November 2021: Dell spins off VMware to its shareholders, making VMware a fully independent company again. This spin-off paved the way for potential suitors to acquire VMware directly.

- May 2022: Broadcom announces an agreement to acquire VMware for approximately $61 billion in cash and stock, one of the largest tech deals ever.

- November 2023: Broadcom completes the acquisition of VMware after regulatory approvals, in a transaction valued around $69 billion including debt. VMware’s stock ceases trading, and VMware is integrated into Broadcom’s software division as “VMware by Broadcom.”

VMware’s Financial Contribution – Before vs. After Acquisition

Broadcom’s FY2024 results (year ended Nov. 3, 2024) illustrate VMware’s impact on the company. VMware was a ~$13–14 billion annual revenue business before the deal (VMware’s last full year as an independent company generated $13.4 billion in revenue). After the acquisition, Broadcom’s infrastructure software segment – which now includes VMware – grew nearly threefold. In FY2024, VMware contributed roughly $13.8 billion of Broadcom’s revenue (almost an entire year of VMware results). The table below compares VMware’s revenue contribution before and after Broadcom’s acquisition:

| VMware Revenue | Before Acquisition (FY2022 standalone) | Post-Acquisition (Broadcom FY2024) |

| Annual revenue (approx.) | $13.4 billion | $13.8 billion |

| % of Broadcom’s total revenue | – (VMware was separate) | ~27% of Broadcom FY2024 revenue |

| Operating margin (VMware business) | ~30% (pre-Broadcom) | ~70% (post-integration) |

Table: VMware’s approximate annual revenue and profitability before vs. after Broadcom’s acquisition. Broadcom’s total FY2024 net revenue was a record $51.6 billion, up 44% year-over-year mainly due to adding VMware. Without VMware, Broadcom’s organic growth was more modest (~low double digits). VMware now represents roughly one-quarter of Broadcom’s revenue, dramatically boosting the software segment. Notably, Broadcom applied its efficiency model to VMware: CEO Hock Tan reported VMware’s quarterly operating costs were cut roughly in half (from $2.4B to $1.2B), increasing VMware’s operating profit margins from under 30% to about 70% post-acquisition. This indicates that under Broadcom’s ownership, VMware’s business has become far more profitable, albeit at the cost of significant restructuring and expense reductions (e.g. layoffs, streamlined R&D). Broadcom is also shifting VMware’s revenue mix toward subscriptions – e.g. promoting VMware Cloud Foundation subscriptions – to drive recurring revenue. VMware’s product segments include compute virtualization (vSphere hypervisor), cloud management and networking (NSX, vSAN), end-user computing (Workspace ONE, VDI), and application modernization (Tanzu). These remained the core streams, but Broadcom is emphasizing long-term subscriptions (“Annual Booking Value”) over up-front licenses. In summary, VMware’s integration has greatly expanded Broadcom’s software revenue and operating profit, while refocusing VMware’s business model toward efficiency and subscription sales.

GAAP vs. Non-GAAP Financial Metrics – FY2024

Broadcom’s FY2024 GAAP results were substantially affected by the VMware purchase accounting. In contrast, Broadcom’s non-GAAP “Industry Standard Reporting” metrics (which exclude certain acquisition-related costs) show the underlying performance. The table below compares key GAAP vs. adjusted metrics for FY2024:

| FY2024 (Broadcom) | GAAP | Non-GAAP (Adjusted) |

| Net Revenue | $51.6 billion | $51.6 billion (no adjustment) |

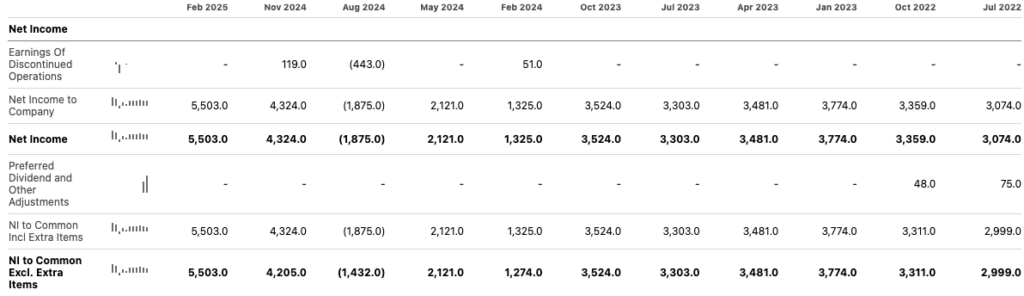

| Net Income | $5.89 billion | $23.73 billion |

| Diluted EPS (annual) | $1.23 | $4.96 |

| P/E Ratio | 160× (very high) | 39× (more normal) |

Table: Broadcom FY2024 GAAP vs. non-GAAP financial results (rounded). P/E is based on year-end trailing earnings. Broadcom’s GAAP net income dropped 58% year-over-year in 2024, despite revenue jumping 44%. GAAP EPS was only about $1.23 (post-split), yielding a P/E over 150×. In contrast, on an adjusted basis Broadcom earned about $4.96 per share, implying a ~40× P/E – still high, but far lower than the GAAP multiple. The stark difference is due to large one-time and non-cash charges related to the VMware acquisition. Broadcom’s non-GAAP figures exclude these items, such as: $9.27 billion of amortization of acquired intangibles (the VMware purchase generated substantial intangible assets like customer relationships to amortize), $5.67 billion of stock-based compensation expense (largely from equity grants and VMware’s pre-merger stock grants being assumed), and $1.79 billion in restructuring costs (severance and integration costs from Broadcom’s aggressive cost-cutting at VMware). These charges pushed GAAP net income down to ~$5.9B even though Broadcom’s cash flows and underlying earnings remained robust.

It’s important to note that Broadcom’s FY2024 GAAP results appear unusual because of these acquisition accounting impacts. For example, amortization of VMware’s intangibles is a recurring GAAP expense for years to come, but it is a non-cash charge that does not reflect ongoing business momentum. The large gap between GAAP and non-GAAP profits in 2024 (GAAP net down 58% vs. non-GAAP net up 29%) underscores this. Investors recognized this dynamic; hence Broadcom’s stock still traded at a high valuation, anticipating future earnings normalization. By FY2025, some metrics will start to normalize – e.g. one-time restructuring costs will disappear, and VMware’s earnings will be fully included for a comparable period. However, GAAP net income will continue to be burdened by amortization of intangibles (Broadcom disclosed that it will amortize VMware-related intangibles over several years). Thus, Broadcom’s GAAP P/E may remain elevated relative to its non-GAAP P/E. In summary, the GAAP vs. NON-GAAP difference in FY2024 is driven by acquisition-related accounting entries rather than core operating performance. Broadcom’s underlying business (as shown by adjusted metrics) grew solidly in 2024, but its GAAP figures were temporarily skewed by the VMware deal. Analysts and investors are aware of these factors, so they focus on adjusted earnings and cash flow, while GAAP figures in FY2024 (and even FY2025) may look “unusual” at first glance due to the VMware purchase accounting.

Other Recent Mergers and Acquisitions

Beyond VMware, Broadcom has executed several other acquisitions in the past five years (excluding any proposed or failed deals):

- Symantec Enterprise Security (2019): In November 2019, Broadcom purchased Symantec’s Enterprise Security business for $10.7 billion in cash. This deal included Symantec’s corporate cybersecurity software products (endpoint protection, network security, etc.) and the rights to the Symantec name, leading Symantec’s remaining consumer division to rebrand as NortonLifeLock. The Symantec enterprise software became part of Broadcom’s infrastructure software segment, expanding Broadcom into security software.

- AppNeta (2021): Broadcom announced in December 2021 its plan to acquire AppNeta, a Boston-based SaaS company specializing in network performance monitoring. The acquisition was completed by February 1, 2022 (terms were not publicly disclosed, but AppNeta had raised around $65M prior). AppNeta’s technology, which provides end-to-end visibility into network traffic from the end-user perspective, was integrated into Broadcom’s “DX NetOps” network monitoring portfolio. This strengthened Broadcom’s software offerings in application and network performance management, complementing its enterprise software from CA.

- ConnectALL (2023): In June 2023, Broadcom acquired ConnectALL, LLC, a provider of value stream management (VSM) software for DevOps teams. (ConnectALL’s platform helps integrate and orchestrate various development and IT tools in the software delivery pipeline.) The deal was completed on June 6, 2023; financial terms were not disclosed, suggesting it was a relatively small tuck-in acquisition. ConnectALL’s technology was added to Broadcom’s “ValueOps” portfolio (which includes Clarity and Rally software from CA) to enhance Broadcom’s agile project management and DevOps tool integrations.

- Seagate SoC Operations (2024): On April 23, 2024, Broadcom (through its Avago Technologies subsidiary) entered an agreement to buy certain system-on-chip assets from Seagate Technology for $600 million. This deal, an asset purchase, transfers Seagate’s in-house silicon design operations (for hard drive controller chips and related IP) to Broadcom. It expands Broadcom’s semiconductor capabilities in storage: Broadcom is a major supplier of HDD and storage controllers, and acquiring Seagate’s SoC design arm likely brings additional IP and talent to Broadcom’s semiconductor division. The transaction also included offers of employment to Seagate engineers and an updated supply agreement, indicating Broadcom will design future storage chips for Seagate.

Each of these acquisitions (Symantec enterprise, AppNeta, ConnectALL, Seagate’s SoC unit, and the landmark VMware deal) reflects Broadcom’s strategy of growth through M&A. Broadcom targets companies that have leading enterprise technologies or complementary semiconductor capabilities, then aggressively integrates and streamlines their operations. This M&A strategy has transformed Broadcom from primarily a semiconductor manufacturer into a diversified infrastructure technology company with significant software, networking, and security product lines.

Revenue Breakdown

Broadcom operates two primary revenue streams: (1) Semiconductor Solutions (mainly hardware products and related IP) and (2) Infrastructure Software (software licenses, subscriptions, and services). Table 1 summarizes Broadcom’s revenues by segment for the fiscal year 2025 (FY2025e, fiscal year ending in late 2024/early 2025) compared to the past five years (FY2019–FY2024), including each segment’s contribution to total revenue and growth rates. All figures are in millions of USD.

| Revenue Stream | FY2019 | FY2020 | FY2021 | FY2022 | FY2023 | FY2024 | FY2025e | FY2025e Share | 5-Year CAGR | YoY Growth |

| Semiconductor Solutions | $17,441 | $17,267 | $20,383 | $25,818 | $28,182 | $30,096 | ~$33,000 | ~55% | +11.6% | +10% |

| Infrastructure Software | $5,156 | $6,621 | $7,067 | $7,385 | $7,637 | $21,478 | ~$27,000 | ~45% | +36.0% | +25% |

| Total Net Revenue | $22,597 | $23,888 | $27,450 | $33,203 | $35,819 | $51,574 | ~$60,000 | 100% | +18.2% | +15% |

Table – Broadcom Annual Revenue by Segment (FY2019–FY2025).

Broadcom’s total annual revenue has grown from ~$22.6 billion in FY2019 to $51.6 billion in FY2024, a ~18% CAGR over five years. This jump in FY2024 reflects the VMware acquisition (closed Nov 2023), which added a large software revenue stream. Excluding acquisition effects, Broadcom’s organic growth has been high-single-digits (e.g. ~9% organic in FY2024). For FY2025, Broadcom is on track for another double-digit increase in total revenue (management guided +19% YoY for Q2 2025), implying roughly $60 billion in full-year revenue (~15% YoY growth).

- Semiconductor Solutions: This segment contributed the majority of revenue historically (around 72–77% of total in FY2019–FY2021). In FY2024, semi solutions were $30.1 billion (58% of $51.6B total). Growth has been steady (FY2019–FY2023 CAGR ~7% organically) and jumped ~7% in FY2024 organically. For FY2025, Semiconductor revenue is forecast to rise about 10% YoY (driven by strong demand for AI-related chips), reaching an estimated ~$33 billion and comprising ~55% of total revenue.

- Infrastructure Software: This segment was much smaller historically ( ~$5–7B annually through FY2019–FY2023, ~23–28% of total). In FY2024 it surged to $21.48 billion (42% of total), nearly 3× higher than FY2023 due to adding VMware’s software business. Excluding VMware, Broadcom’s existing software lines grew ~9% in FY2024). Going into FY2025, software revenues are expected to continue climbing (Q1 FY2025 software was up +47% YoY including VMware). We project Infrastructure Software around ~$27 billion for FY2025 (roughly +25% YoY, about 45% of total revenue), reflecting a full year of VMware ownership and modest organic growth in legacy software.

In summary, Broadcom’s revenue mix is now roughly half semiconductor and half software. This is a shift from five years ago when semiconductors constituted the vast majority of sales. The VMware deal transformed Broadcom’s portfolio, boosting the software segment from under $8B to over $21B annually. Despite this diversification, Broadcom’s core chip business remains on a growth trajectory (especially in networking and AI silicon), while the expanded software division contributes a significant portion of new revenue and recurring subscription streams. The overall company is expected to sustain double-digit revenue growth into FY2025, fueled by record demand in AI-related semiconductors and the integration of VMware.

Business Segment Analysis

Broadcom’s two revenue streams encompass multiple business segments and product lines. Below, we break down each stream into its key segments, discussing Broadcom’s products, market performance, and development history in each, followed by a competitive analysis table comparing Broadcom’s offerings to peers.

Semiconductor Solutions

Broadcom’s Semiconductor Solutions segment includes all its hardware product lines and associated IP. These products manage the movement of data across networks, devices, and storage, and serve a broad range of end markets – from data center networking and wireless communications to broadband, enterprise storage, and industrial applications. In FY2024, this segment generated $30.1B (58% of total revenue), a record high driven largely by demand for networking chips (especially those used in AI infrastructure). The Semiconductor segment’s major business sub-segments are detailed below:

Networking ASICs (Switches & Routing, including AI Networking)

Broadcom is a market leader in data center networking silicon, producing switch and router ASICs under families like Trident, Tomahawk, and Jericho, as well as network interface controllers (NICs) and custom application-specific ICs. These chips are critical for Ethernet switching in cloud and enterprise data centers and for connecting servers in high-bandwidth environments. Broadcom’s networking ASICs have dominated the merchant silicon market – the company long held ~70% share in Ethernet switch chips (down from >90% in 2015 as competitors emerged). In 2022, Broadcom and one other supplier (Marvell via Innovium) were the top two providers of merchant switch silicon. Broadcom’s latest Tomahawk 5 and Jericho3-AI chips deliver industry-leading throughput (25.6–51.2 Tbps switching capacity) and cutting-edge SerDes speeds (112G/224G), enabling cloud giants to scale their networks.

– Product Performance & History: Broadcom’s networking silicon lineage began with the original Broadcom Corp (acquired by Avago in 2016), which pioneered high-integration Ethernet switch chips in the 2000s. Successive generations (Trident for enterprise, Tomahawk for cloud-scale switching, Jericho for routing) have set performance benchmarks. In recent years, Broadcom has extended its portfolio to AI networking – providing custom AI accelerator chips (so-called “XPUs”) and ultra-high bandwidth connectivity ASICs for hyperscale cloud customers. In FY2024, networking was Broadcom’s largest semiconductor sub-segment, with Q4 networking revenue of $4.5B (up 45% YoY). Notably, AI-related networking (custom AI processors and associated switch chips) made up 76% of Broadcom’s Q4 networking sales and grew 158% YoY, fueled by cloud firms like Google, Meta, and others ramping in-house AI infrastructure. Broadcom reported $12.2B in AI-driven semiconductor revenue for FY2024, a surge of 220% from $3.8B in FY2023. This underscores Broadcom’s successful pivot to servicing AI data center needs, on top of its steady business in conventional network chips.

– Competitive Landscape: Table compares Broadcom’s networking ASIC offerings with key competitors. Broadcom’s main challenger in merchant switching is Marvell Technology, which acquired Innovium and Cavium to bolster its Ethernet switch and custom ASIC capabilities. NVIDIA (via its Mellanox acquisition) is another peer, focusing on NICs, InfiniBand and DPU (data processing unit) solutions for high-performance computing. Additionally, Intel (through its Barefoot Networks tech) has attempted programmable switch ASICs, and system vendors like Cisco internally develop some networking ASICs for their own switches. Broadcom’s competitive advantage lies in its scale and integration – it offers proven, full-featured switching platforms with the highest performance, and has deep relationships supplying all major OEMs and cloud operators. Its Tomahawk/Jericho series are often the default choice for data center switching, whereas competitors target niche or next-tier opportunities. Marvell’s Teralynx (from Innovium) competes in cloud switching but has a smaller adoption, and NVIDIA’s focus is on specialized networking (InfiniBand and smart NICs) rather than broad Ethernet switching. Broadcom’s custom ASIC business also benefits from its ability to co-design silicon with hyperscalers; for instance, it manufactures Google’s TPU AI chips and others – J.P. Morgan estimates Broadcom has ~55–60% share in the custom silicon market for AI accelerators. One disadvantage for Broadcom is the emerging trend of large cloud customers developing in-house silicon, which introduces the risk of future designs not using Broadcom chips (though currently Broadcom often wins the contract to fab those in-house designs). Overall, Broadcom’s networking products enjoy a strong incumbency and performance lead, particularly in Ethernet switching, but face growing competition as alternative vendors and architectures (like NVIDIA’s InfiniBand or cloud-native designs) vie for share.

| Networking ASICs | Broadcom – Tomahawk / Jericho / Custom ASICs | Marvell – Prestera / Teralynx / Custom ASICs | NVIDIA – Mellanox Spectrum / InfiniBand |

| Market Position | Leader – ~70% share in DC Ethernet switching ASICs; Supplier to major OEMs (Cisco, Arista) and cloud players. Also ~55% share in custom AI silicon | Challenger – Gained high-speed switch ASIC tech via Innovium (Teralynx). Competes for cloud designs; smaller share vs Broadcom. | Specialist – Focus on InfiniBand and NICs for HPC; Spectrum Ethernet switches have niche use in supercomputing, not mass-market cloud switching. |

| Flagship Products | Tomahawk 5 (51.2 Tbps switch), Jericho3-AI (routing & AI cluster switching), NICs (NetXtreme). Custom 7nm/5nm AI chips for hyperscalers (Google TPU, etc.). | Teralynx 8 (25.6 Tbps switch) from Innovium; Prestera switches for enterprise; custom ASIC offerings via 5nm platform (Octeon infrastructure processors). | Spectrum-4 (celestial 51.2 Tbps Ethernet switch) and Quantum-2 InfiniBand. BlueField DPUs (Smart NICs) for offload. Acquired Cumulus for NOS software integration. |

| Comparative Strengths | Highest-performance Ethernet switch silicon; broad feature support (deep buffers, programmable pipelines). Long history of stable software (SDK) that OEMs integrate. Can execute large custom ASIC projects (mixing networking and compute). Economies of scale in R&D. | Competitive port speeds and power efficiency on select cloud-focused chips (Innovium design). Marvell offers both standard products and will do semi-custom. Strong in specific niches (carrier, embedded networking from Cavium heritage). | Leadership in ultra-low-latency and HPC networking (InfiniBand). Strong coupling of NIC + switch for AI clusters. Offers end-to-end networking solution (DPUs, switches, cables) optimized for GPU systems (popular in AI clusters not using Ethernet). |

| Comparative Weaknesses | Highly dependent on cloud capex cycles and standards (Ethernet). Faces risk from in-house silicon at big cloud customers. Minor competition pressure on pricing from second sources (Marvell). | Lacks the broad product portfolio of Broadcom; fewer generations proven in field. Much smaller software ecosystem support compared to Broadcom’s well-established API/SDK. | Limited presence in general cloud switching (Ethernet); primarily sells where InfiniBand is needed (HPC) or where customers adopt NVIDIA’s full-stack. Not a direct drop-in replacement for Broadcom in most large networks. |

Table – Competitive Comparison: Broadcom vs. Peers in Networking ASICs. Broadcom dominates data center switching chips, with Marvell and NVIDIA pursuing specific segments. Broadcom’s end-to-end Ethernet solutions and custom silicon capabilities give it a broad advantage, particularly as AI workloads drive demand for high-bandwidth networking.

Wireless Communications (RF & Connectivity)

Broadcom supplies critical wireless components for smartphones and mobile devices, most notably RF front-end modules (RF filters, amplifiers) and combo connectivity chips (Wi-Fi + Bluetooth). Broadcom’s Wi-Fi/Bluetooth silicon is used in billions of devices – it is a leading provider of Wi-Fi 6/6E and emerging Wi-Fi 7 chipsets for smartphones, laptops, and access points. In RF, Broadcom is known for its premium FBAR (Film Bulk Acoustic Resonator) filters that enable reliable 4G/5G wireless frequency filtering. The company’s largest customer in this arena is Apple Inc., which relies on Broadcom for several key chips in the iPhone (e.g. Wi-Fi/Bluetooth radio, RF filter modules, wireless charging controllers, touch controllers). In FY2024, Broadcom’s Wireless sub-segment saw a seasonal peak in Q4 (Apple’s iPhone launch) with $2.2B revenue in the quarter, up 7% YoY due to increased Broadcom content per phone. Annual wireless revenue tends to track smartphone cycles; Broadcom benefits from multi-year design wins at Apple and others. Historically, Broadcom (Avago) built this franchise by acquiring companies like NetLogic and Broadcom Corp’s connectivity division (2016), and has since focused on high-performance filters and connectivity chips rather than cellular modems.

– Product Performance & History: Broadcom’s Wi-Fi/Bluetooth combo chips are considered best-in-class in terms of integration and performance, often beating out peers in power efficiency and new protocol adoption. For instance, it was among the first to deliver Wi-Fi 6E chipsets to handset makers. Its FBAR RF filters (originating from Avago’s HP heritage) command a technological edge in filtering precision at high frequencies (critical for 5G bands). These advantages have allowed Broadcom to secure a large share of the RF content in premium smartphones. However, a notable development is Apple’s plan to in-source some of these components: Apple has announced it intends to replace Broadcom’s Wi-Fi/Bluetooth chip with an in-house design by 2025. Apple represents about 20% of Broadcom’s total revenue, so the potential loss of this socket (worth an estimated $1–1.5B in revenue) is a medium-term risk. Broadcom’s RF front-end chips (like RF filters) are expected to remain in Apple devices in the near term, as those are more complex to replace. Beyond Apple, Broadcom provides wireless chips to other handset OEMs and for Wi-Fi access points, though Apple’s volume dominates this business. Broadcom has also developed niche wireless solutions (e.g. custom touch controllers and wireless charging ICs used in smartphones), showcasing its ability to cross-sell multiple chip types into the same device.

– Competitive Landscape: The wireless component market is highly competitive, with specialized players. Qorvo and Skyworks are Broadcom’s main competitors in RF front-end modules (filters, amplifiers), while Qualcomm and MediaTek compete in Wi-Fi/Bluetooth connectivity chips (often bundled with their mobile SoCs). Table highlights a comparison. Broadcom’s strength is its technology leadership in FBAR filters (for which competitors largely use SAW/BAW filtering with slightly lower performance) and its integration of Wi-Fi/BT into a single combo chip solution widely regarded as top-tier. Broadcom’s solutions tend to command a price premium. Qorvo and Skyworks, by contrast, focus on a broad range of RF components and serve more diversified customer bases (Android OEMs, mid-tier phones) – they have sometimes won designs where Broadcom was absent or when cost sensitivity is higher. In connectivity SoCs, Qualcomm often integrates Wi-Fi/BT into its Snapdragon mobile processors for Android devices, reducing the TAM for Broadcom in those phones. Broadcom’s comparative advantage is evident in the premium segment (e.g. iPhones) where performance is paramount and multi-chip integration is valued; its disadvantage is that it relies heavily on a few flagship customers and does not offer cellular baseband chips (so it cannot offer a one-stop handset platform the way Qualcomm can). With Apple aiming to self-supply some chips, Broadcom is focusing on staying ahead in RF technology and expanding into new wireless opportunities (it has hinted at working with Apple on next-gen Wi-Fi 7/Bluetooth and continues to develop advanced RF for 5G/6G).

| Mobile Wireless Components | Broadcom – Wi-Fi/Bluetooth & FBAR RF | Qorvo – RF Systems | Skyworks – RF Front-End | Qualcomm – Connectivity SoCs |

| Product Focus | Premium Wi-Fi/Bluetooth combo chips; high-performance RF filters (FBAR); custom wireless charging and touch ICs. | RF front-end modules (BAW filters, power amplifiers, antenna tuners) for mobile, defense, Wi-Fi, etc. Limited connectivity silicon (some Wi-Fi via acquisitions). | RF front-end modules (filters, PAs, switches) for mobile and IoT. Focus on high-volume smartphone RF content. | Complete mobile SoC including integrated Wi-Fi, Bluetooth, GPS in Snapdragon; standalone Wi-Fi/BT chips for certain markets; cellular basebands. |

| Market Position | Leader (premium segment) – Supplies virtually 100% of Wi-Fi/BT combos to high-end phones like Apple iPhone (with top performance). Major RF module supplier for iPhone (coexisting with Skyworks). | Major RF supplier – One of top 3 RF players (with Skyworks & Broadcom). Strong presence in Android phone RF front-ends, infrastructure and defense RF. | Major RF supplier – High-volume RF component provider, particularly to Apple (historically) and many Android models. Often chosen for complete front-end solutions. | Mobile platform leader – Dominant in smartphone modems and application processors; its built-in connectivity captures most of Android high-end, making an external Broadcom combo less necessary in those devices. |

| Tech/Performance | FBAR filters offer superior filtering at high bands (Broadcom’s niche) Wi-Fi 6/6E/7 solutions with cutting-edge MIMO, low power. Strong custom solutions (e.g. first to support Wi-Fi 6E in phones). | Solid BAW filter technology (from TriQuint) but seen as slightly behind Broadcom’s FBAR at some bands. Broad portfolio of PAs and switches. Integrates modules for 5G phones (not significantly behind Skyworks/BRCM in performance). | Known for highly integrated modules (SkyOne, etc.) combining filter/PA/switch for ease of design. Uses BAW/SAW filters; performance competitive, though Broadcom often wins on toughest specs. | Wi-Fi/BT typically one generation behind Broadcom when integrated (e.g. Qualcomm’s standalone or integrated Wi-Fi 6E appeared after Broadcom’s). Good enough for most uses; tight integration with the Snapdragon SoC yields power and cost efficiencies in Android devices. |

| Comparative Strengths | Best-in-class filter tech yields content wins in premium 5G phones (can meet stringent RF specs). Long-term partnership with Apple (multiple chips in iDevices). Wi-Fi/Bluetooth combos have broad adoption beyond phones (enterprise APs, game consoles, etc.). | Broad RF catalog and ability to serve multiple markets (not dependent on one customer). Strong in defense/aerospace RF (diverse revenue). Merged from TriQuint & RFMD, has scale. | Turnkey RF front-end solutions to phone OEMs, easing design. Historically strong at Apple (supplied PAs/filters alongside Broadcom). Focused solely on RF, so deeply specialized. | Offers a complete solution (apps processor + modem + connectivity), giving OEMs convenience and lower total cost for Android handsets. Massive R&D in wireless standards (5G/6G) flows into its connectivity IP. |

| Comparative Weaknesses | Customer concentration (20% of rev from Apple); at risk if Apple’s in-house chip succeeds (loss of Wi-Fi/BT socket by 2025) | Less exposure to the very high-end filters (some OEMs prefer Broadcom for hardest bands). No presence in connectivity SoCs – depends on partners for Wi-Fi/Bluetooth. | Limited R&D budget compared to Broadcom; no connectivity or digital processing products – purely analog RF, which could be commoditized over time. Apple has shifted some content away at times. | Its discrete Wi-Fi/BT chips (when offered) are generally not as advanced as Broadcom’s; primarily focused on integrated solutions which may not push standalone performance envelope. Not a direct RF competitor (relies on partners like TDK for filters) |

Table – Competitive Comparison: Broadcom vs. Peers in Mobile Wireless Components. Broadcom’s wireless business (Wi-Fi/Bluetooth chips and RF modules) is differentiated by high performance and key design wins (especially Apple). Qorvo and Skyworks rival Broadcom in RF components for mobile devices, while Qualcomm competes by integrating connectivity into its mobile platforms.

Broadband & Networking Access

Broadcom provides system-on-chip (SoC) solutions for broadband access and set-top boxes, including chips for cable modems, fiber/DSL gateways, and video streaming devices. These products stem from the legacy Broadcom and STMicroelectronics businesses (Broadcom acquired Brocade’s networking and also inherited LSI’s broadband line). Broadcom’s Broadband category covers chips used by service providers in customer premises equipment (home internet gateways, GPON/DSL modems) and by cable/satellite companies in set-top decoders. In FY2024, Broadband was a smaller portion of the semi segment – Q4 broadband revenue was $465M (around 6% of Q4 semi) and was down 51% YoY due to a cyclical inventory correction at customers. This indicates the broadband chip business can be volatile, driven by upgrade cycles (e.g. transition to DOCSIS 4.0 or fiber rollouts). Broadcom has a strong position in DOCSIS (cable modem) silicon and in DSL chipsets (via the earlier Broadcom Corp). It also produces Ethernet PHY chips and switching chips for broadband access (these complement its core switching line).

– Product Performance & History: Broadcom’s broadband access chips have been in the market for decades and are found in many home gateways. The company often leads in introducing new standards support (for example, early DOCSIS 3.1 modem SoCs, and now working on DOCSIS 4.0). In set-top boxes, Broadcom SoCs power video decoding and smart TV features for many cable and satellite TV providers worldwide. However, this market has matured and even declined with the shift to streaming. Broadcom’s strategy has been to continue offering full-platform solutions for the remaining pay-TV providers and to capture new business in fiber access (the company’s PON optical line terminal/ONT chips are used by telecom operators for fiber-to-home networks). The historical development includes acquisitions like SeaGate’s networking (for DSL) and Home Networking business from Broadcom Corp. Broadcom’s broadband products are a stable, if not high-growth, part of the portfolio, providing steady cash but subject to end-market declines (e.g. fewer new set-top box deployments as cord-cutting rises). FY2024 likely marked a trough, and management noted an expected recovery in broadband starting Q1 FY2025 as orders picked up again.

– Competitive Landscape: In broadband and access chips, Broadcom competes with companies like MaxLinear (which offers cable modem and broadband SoCs, and had even agreed to acquire Intel’s Home Gateway division), MediaTek (supplies TV and some broadband chipsets), and Intel (historically in cable modems, though Intel’s cable unit was to be sold to MaxLinear). Table outlines the comparison. Broadcom’s advantage is its comprehensive product lineup and incumbency with major operators – it’s often the default choice for cable companies (Comcast, etc.) for both modem and set-top silicon. MaxLinear has been a nimble competitor, sometimes undercutting on cost or specializing in certain areas like frontier OFDM technology for cable. MediaTek competes more on the consumer side (e.g. smart TV chips, some lower-end OTT box chips) and less so in infrastructure-grade modems. Broadcom’s SoCs tend to be high performance and robust, but the company is less focused on low-cost markets. One disadvantage Broadcom faces is the overall slow growth or decline in some of these segments – for example, if cable operators reduce hardware deployments, Broadcom’s addressable market shrinks. Additionally, the rise of open-source or standardized network gear could open doors for other chip vendors. Still, Broadcom’s long-standing relationships and complete solutions (including reference designs and software SDKs for gateway boxes) give it a competitive moat.

| Broadband Access Chips | Broadcom – Cable Modem/DSL/Set-Top SoCs | MaxLinear – Broadband & Video SoCs | MediaTek – TV & Broadband Silicon |

| Key Products | DOCSIS cable modem SoCs (BCM33xx series), xDSL and PON fiber access chipsets, Wi-Fi router SoCs, Set-top box SoCs (video decoders). Ethernet PHYs and switches for broadband CPE. | Cable modem and MoCA chips (from Intel Home Gateway acquisition), satellite TV tuner chips, video compression ICs (via Sigma Designs). Wired broadband transceivers. | IPTV/set-top processors, Smart TV SoCs, some DSL and Wi-Fi router chips (often targeting cost-sensitive consumer devices). Also mobile chip expertise applicable to TV boxes. |

| Market Focus | Serves major cable/MSOs (Comcast, Charter) and telcos for subscriber premises equipment. Strong in North America and Europe cable markets. Also provides reference software for set-top. | Focus on broadband operators as well, with strength in satellite/cable tuner tech. Competes for cable modem sockets especially in value segments. Also serves niche video markets (broadcast). | Focus on consumer electronics: smart TVs (many top TV brands use MediaTek), Android TV boxes, etc. Less present in operator-provided gateways, more in retail or OEM devices. |

| Competitive Strengths | End-to-end solution provider (from optical to modem to Wi-Fi in home). Very mature, reliable solutions; long-term support commitments which operators require. Leading performance in cable modems (early DOCSIS 4.0 demos). | Aggressive pricing and fast implementation of new features (e.g. first with certain low-power tuner designs). Fabless with lower cost structure, appealing to price-conscious operators. Diversified (tuner, modem, interface chips). | High-volume consumer market experience – very cost-efficient designs. Strong multimedia performance in SoCs (leverages mobile GPU/CPU tech for OTT boxes). Close ties with Asian device manufacturers. |

| Competitive Weaknesses | Broadband market growth is low – reliant on upgrade cycles. Some customers exploring open hardware. Broadcom may be less interested in low-margin deals. Also faced supply constraints in past that could push customers to second source. | Much smaller scale than Broadcom; limited ability to support massive deployments alone. Tried to merge with Silicon Motion (failed) – somewhat fragmented portfolio. Dependent on foundries Broadcom also uses. | Less focused on carrier-grade reliability or software support for operators. Not a traditional supplier to big cable/telco (except when those operators use consumer-grade gear). Faces intense competition in commodity TV chip market. |

Table – Competitive Comparison: Broadcom vs. Peers in Broadband Access Semiconductors. Broadcom’s broadband SoCs are entrenched with major cable/telco operators, whereas rivals like MaxLinear compete on cost and specific features. MediaTek plays more in consumer/OTT devices than carrier-grade equipment.

Server Storage & Connectivity

Broadcom supplies a broad array of enterprise storage and connectivity chips. This includes RAID controllers, storage adapters, PCIe switch chips, and Fibre Channel network chips used in servers and storage systems. Many of these products came via Broadcom’s LSI Corp. acquisition and Emulex/Brocade acquisitions. Broadcom’s offerings here enable data to move between servers and storage devices (e.g. its MegaRAID controllers manage HDD/SSD arrays, its PCIe switches connect NVMe devices, and its Emulex host bus adapters enable Fibre Channel SAN access). In FY2024, Broadcom saw a downturn in enterprise storage in early 2024, but by Q4 server/storage connectivity revenue had rebounded ~20% off the bottom to $992M in the quarter. This segment tends to follow enterprise IT spending cycles. Broadcom is a leading vendor in Fibre Channel (FC) technology via its Brocade switches and Emulex adapters – in fact, it’s one of two primary FC providers (with Cisco). It also dominates in certain types of RAID controllers and SAS (Serial Attached SCSI) infrastructure chips for data centers.

– Product Performance & History: Broadcom (formerly Avago/LSI) has been in the storage controller business for decades, with its chips widely used in servers (e.g. Dell, HPE use Broadcom/LSI RAID-on-chip for internal storage management). It has continuously updated these for new standards (e.g. supporting SAS-4, PCIe Gen4/5). The company’s Fibre Channel switches (Brocade line) are the backbone of many storage area networks in enterprise datacenters, maintaining a robust niche despite the rise of Ethernet-based storage, because mission-critical applications still use FC for reliability and low latency. Broadcom’s FC switch business (reported under Infrastructure Software segment historically, as it includes hardware+software solutions) has a high market share alongside Cisco’s MDS switches. In adapters (connecting servers to either Ethernet or FC), Broadcom’s Emulex division (and NetXtreme Ethernet NICs) compete with others like Marvell (QLogic) and Intel. Over the years, Broadcom has expanded through acquisition in this arena – e.g., buying Emulex (2015) for Fibre Channel HBAs, Brocade (2017) for FC switches, and LSI (2014) for RAID/storage controllers. These products are typically high-margin and sticky, as enterprise customers require long support and proven interoperability (which Broadcom provides). In FY2024, as enterprise spending on servers slowed, Broadcom’s storage segment dipped, but is expected to recover alongside server demand in 2025. Broadcom’s introduction of newer PCIe Gen5 switches and NVMe storage controllers is positioned to capture growth in all-flash arrays and NVMe-over-fabrics trends.

– Competitive Landscape: Key competitors in server/storage connectivity include Marvell Technology (which owns QLogic Fibre Channel adapters and offers Ethernet NICs and storage controllers after acquiring Cavium), Intel (in Ethernet adapters and some SSD controllers), and niche players like Microchip (which acquired Microsemi/Adaptec for some RAID controllers). Table compares Broadcom with Marvell and Microchip. Broadcom’s clear advantage is the breadth of its portfolio – it is the only one offering end-to-end solutions from Fibre Channel SAN switches to HBAs to RAID chips. Marvell competes in many of the same areas (Marvell’s QLogic is the #2 in FC adapters, and Marvell offers its own line of PCIe switches and storage SoCs), but Marvell does not sell Fibre Channel switches (only adapters). Microchip, via Adaptec and PMC-Sierra, has some presence in SAS controllers and Flash controllers, but is smaller. Broadcom’s products are often regarded as the gold standard in reliability (important for enterprise). However, Broadcom’s focus on high-end may leave some low-end niches where competitors undercut. For example, Marvell has Ethernet-based storage adapter solutions and has been investing in NVMe-oF controller tech that could challenge Broadcom’s older SAS/SATA focus. Broadcom’s comparative strength is incumbency and integration – OEMs can get a turnkey suite of storage connectivity from Broadcom. A comparative weakness is that new paradigms (like software-defined storage on Ethernet networks) could reduce reliance on specialized hardware like RAID controllers or Fibre Channel gear over time. Broadcom is responding by also offering solutions for NVMe (it has NVMe switch chips and is integrating compute offloads on its NICs for storage tasks).

| Server & Storage Connectivity | Broadcom – RAID, FC & NIC Solutions | Marvell – QLogic & Storage Chips | Microchip – Adaptec & SAS Solutions |

| Product Lines | RAID controllers (MegaRAID), SAS/SATA HBAs, PCIe switches (PEX series for connecting GPUs/SSDs), Ethernet NICs (NetXtreme), Fibre Channel HBAs (Emulex LPe series), Fibre Channel switches (Brocade SAN directors). | Fibre Channel HBAs (QLogic brand, second to Broadcom Emulex), Ethernet NICs/DPUs (Marvell FastLinQ, Octeon Smart NICs), PCIe switches (offers own Prestera switches for PCIe fabrics), Storage processors for SSD controllers (Marvell is big in flash controllers), some SAS expanders. | RAID adapters (Adaptec SmartRAID series), SAS expanders and controllers (from PMC-Sierra acquisition), some PCIe switch products, and timing/clocking chips for storage. Primarily focusing on SAS/SATA infrastructure and niche storage controllers. |

| Market Share/Position | Leader – #1 in RAID controllers (over 80% share with OEMs), #1 in Fibre Channel (both switches: ~70% share, and HBAs: ~50+% share) | Challenger – #2 in FC adapters (QLogic), competes closely in Ethernet NICs (especially smart NICs for cloud), #2 in some storage controllers. Strong presence in flash/SSD controllers (used by SSD makers). | Challenger – #2 in FC adapters (QLogic), competes closely in Ethernet NICs (especially smart NICs for cloud), #2 in some storage controllers. Strong presence in flash/SSD controllers (used by SSD makers). |

| Strengths | Complete ecosystem for SAN storage (only vendor for FC switches). Highly trusted by OEMs – long-term backwards compatibility and software support (drivers, management tools) across generations. Continual innovation in high-bandwidth interconnects (e.g. early PCIe Gen5 switch deployment). | Broad portfolio in both storage and networking; can offer Ethernet-centric solutions that Broadcom doesn’t emphasize (e.g. NVMe-oF accelerators). Good traction in cloud/hyperscale storage (Marvell provides custom silicon to some SSD and HDD manufacturers). Aggressive in new tech (early DPUs, etc.). | Focused expertise in SAS/SATA – their controllers often second source to Broadcom in servers, ensuring competition. Strong in timing and signal integrity components (Microchip has Microsemi timing solutions that complement storage networks). Often chosen when an independent second supplier is needed for regulatory or risk reasons. |

| Weaknesses | Fibre Channel market is flat/declining long-term; Broadcom’s dominance in legacy protocols may not carry over if Ethernet or NVMe-over-TCP/IP takes over storage networking. Also, Broadcom’s high-end focus can mean less attention to low-cost or niche products. | No presence in FC switching (relies on Broadcom’s existence in market). Integration of various acquired pieces (QLogic, Cavium) still ongoing – not as seamless as Broadcom’s lineup. Market share in RAID is low after OEMs standardized on Broadcom; hard to displace without heavy incentives. | Very limited portfolio breadth – cannot offer complete solution (e.g. no NIC or FC products). Much smaller R&D budget, meaning slower to new standards (lagged Broadcom in releasing PCIe Gen4/5 SAS controllers). Often relegated to legacy or cost-sensitive designs. |

Table – Competitive Comparison: Broadcom vs. Peers in Server/Storage Connectivity. Broadcom holds a dominant position in enterprise storage connectivity (RAID controllers, Fibre Channel). Marvell is a strong competitor in adapters and is pushing into Ethernet-centered storage solutions, while Microchip serves as a niche alternative in SAS/SATA connectivity.

Industrial and Automotive

Broadcom also sells various industrial and automotive oriented components – for example, optocouplers, motion encoders, LED displays, and some automotive-grade custom ASICs. This is the smallest sub-segment (only ~1% of Broadcom’s revenue). In Q4 FY2024, industrial segment revenue was $173M (down 27% YoY amid broader industrial semiconductor softness). Broadcom’s history in this space comes from legacy HP/Avago products (optoelectronics used in factory automation, isolation amplifiers, etc.) and some later additions. While tiny in contribution, these products often have high margins and stable demand in niche applications. Competitors here are diverse (ranging from Vishay and Renesas in optocouplers to smaller analog chipmakers), but Broadcom’s presence is relatively limited and focused on areas where it has unique IP. For instance, Broadcom’s optical isolators are well-regarded for reliability in power systems. In automotive, Broadcom supplies some connectivity chips (it was a pioneer in Ethernet for cars with its BroadR-Reach technology, now part of automotive Ethernet standards). Overall, this segment is not a major focus for growth, and Broadcom expects a recovery only in the second half of FY2025 for industrial demand. It remains a small, steady contributor with little direct impact on Broadcom’s strategic direction.

Infrastructure Software

Broadcom’s Infrastructure Software segment includes all the software solutions the company offers, spanning enterprise software, mainframe/software infrastructure, cyber-security, and SAN equipment software. This segment was built via major acquisitions: CA Technologies (2018) gave Broadcom a portfolio of mainframe and enterprise software, Symantec’s Enterprise Security division (2019) added cybersecurity software, and most recently VMware (2023) added cloud and virtualization software. In FY2024, Infrastructure Software revenue was $21.48B (42% of total) – nearly triple the prior year’s level due to VMware’s inclusion. Broadcom’s strategy in software has been to acquire mature, “mission-critical” software platforms with loyal enterprise customer bases, then optimize their operations and cross-sell to large clients. Below we break out the major components of this segment:

Virtualization and Cloud (VMware)

This is Broadcom’s newest and largest software business, acquired in November 2023. VMware is a leading provider of enterprise virtualization software – its flagship vSphere platform virtualizes servers, allowing multiple workloads on one physical machine, which became a de facto standard in data centers. VMware also offers multi-cloud and hybrid cloud solutions (vRealize, CloudFoundation), networking and security virtualization (NSX), storage virtualization (vSAN), and modern application platforms (Tanzu for containers). VMware had an enormous installed base of ~375,000 customers as of 2024, including most Fortune 500 companies. Under Broadcom, VMware contributed ~$15 billion+ to FY2024 software revenue (since Broadcom had ~$7B software pre-VMW, now $21.5B total). Broadcom has focused VMware on its core strength of data center virtualization and is packaging its products into a comprehensive offering (VMware Cloud Foundation, a bundle for private/hybrid cloud). Broadcom’s CEO Hock Tan noted that VMware’s operating margin was driven up to ~70% by the end of FY2024 through cost optimizations.

– Market Performance & History: VMware pioneered server virtualization in the early 2000s and grew consistently as enterprises sought to improve IT efficiency. By the time of acquisition, VMware’s annual revenue was around $13 billion and growing in mid-single digits. In the broader market, VMware faces competition from the public cloud (AWS, Azure) as some workloads migrate off-premises, and from open-source virtualization/containerization (like KVM, Docker, Kubernetes) as alternatives to proprietary VMware tech. Nevertheless, VMware’s products remain deeply embedded in enterprises (especially for private clouds). Broadcom’s approach has been to monetize VMware’s strong position by consolidating products and implementing substantial price increases for comprehensive suites. Gartner reported some customers seeing up to 5× price hikes for VMware under Broadcom’s regime. This has caused some customer pushback – e.g., AT&T filed a suit in 2024 alleging Broadcom forced it into unwanted software purchases. Despite these headwinds, Broadcom asserts that VMware’s revenue is on a growth trajectory under its ownership, with key metrics like Annualized Booking Value (ABV) rising – VMware’s Q4 FY2024 ABV was $2.7B, up from $2.5B in Q3, indicating strong bookings. Broadcom is prioritizing VMware’s large customers (it signed 4,500 of the top 10k customers onto VMware Cloud Foundation bundles in the first year) and appears willing to let some smaller clients drop off. This strategy mirrors Broadcom’s past approach with CA and Symantec: focus on the biggest 500-1000 customers that contribute the bulk of revenue, even if some smaller accounts churn.

– Competitive Landscape: VMware’s main competitors include Microsoft (with Hyper-V virtualization and Azure Stack for hybrid cloud), Red Hat/IBM (with KVM and OpenShift virtualization/container solutions), and the general shift to public cloud services (which can eliminate the need for on-prem VMware in some cases). Table compares VMware (under Broadcom) with some peers. VMware’s strength has always been its feature richness and integration: it offers not just hypervisors, but a full suite (network, storage virtualization, management tools) that works across different hardware and clouds. Microsoft’s Hyper-V is bundled with Windows Server (making it cost-attractive) but has a smaller ecosystem. Public clouds (AWS, etc.) compete by offering elasticity and native services, though VMware has partnerships to run VMware Cloud on AWS/Azure for customers wanting the best of both. Under Broadcom, VMware’s advantage is a renewed focus and investment in core R&D (Broadcom has indicated it will continue to develop VMware technology leadership), plus Broadcom’s financial discipline which ensures profitability. A perceived disadvantage could be customer relations – some CIOs worry Broadcom will be less flexible or more expensive, driving them to evaluate alternatives. Already, Gartner suggests CIOs assess their risk and consider other platforms post-acquisition. However, fully migrating away from VMware can be costly and complex for enterprises, which gives Broadcom a degree of pricing power. Overall, VMware remains the market leader in on-premises virtualization by market share. The question is how it competes in the era of hybrid cloud: VMware is developing offerings like VMware Cloud Foundation and Tanzu (Kubernetes) to stay relevant. Broadcom’s challenge (and opportunity) is to leverage VMware’s dominance in private data centers to capture spend from companies pursuing hybrid cloud strategies, while fending off competition from cloud providers and open-source alternatives.

| Enterprise Virtualization & Cloud | VMware (Broadcom) | Microsoft (Azure/Hyper-V) | Open-Source/Other (KVM, etc.) |

| Market Position | Leader in private cloud virtualization. VMware vSphere holds dominant share of enterprise hypervisors in on-prem data centers. Strong hybrid cloud play via VMware Cloud on AWS/Azure. Now under Broadcom, refocused on top global 1000 customers and high-value deals | Major competitor (bundled). Hyper-V is widely used as part of Windows Server; Microsoft Azure Stack allows on-prem Azure-consistent environment (competes with VMware Cloud Foundation). Microsoft leverages enterprise Windows footprint to push Hyper-V, though its share is smaller than VMware in virtualization. | Alternative solutions. KVM (open-source hypervisor used by many Linux-based clouds) and Xen are free alternatives; OpenStack and Red Hat OpenShift provide open cloud frameworks. Often adopted by cost-sensitive or highly tech-savvy organizations. Lacks VMware’s comprehensive features but improving. |

| Product Scope | Full suite: vSphere (ESXi hypervisor + vCenter management), NSX (network virt.), vSAN (storage virt.), Tanzu (containers), Cloud Foundation (integrated stack). Supports multi-cloud management and migration tools. Broadcom emphasizes bundled sales of entire stack for private cloud | Hyper-V hypervisor (part of Windows), System Center for management, Azure Stack HCI for hybrid cloud integration. Strong integration with Windows and Azure services (e.g., easy VM migration to Azure). Less comprehensive virtualization-specific networking/storage features than VMware (makes up via Azure services). | KVM is a core hypervisor integrated into Linux distributions; Proxmox or Ovirt for management; OpenStack for full cloud management; Red Hat Virtualization/OpenShift for enterprise support on KVM and container management. Very flexible and no license cost, but requires more integration effort. |

| Strengths | Unmatched feature depth and reliability in enterprise virtualization (VMware is the gold standard for running mixed enterprise workloads). Huge installed base and third-party ecosystem (tools, certified hardware). Broadcom’s ownership brings strong financial backing and a focus on R&D efficiency (already 70% op margins achieved)). VMware also provides consistency across on-prem and cloud (via VMware Cloud offerings), easing hybrid deployments. | Deep integration with enterprise IT (Windows/AD/Office). Hyper-V comes essentially “free” with Windows Server, which appeals to cost-conscious shops. Azure’s dominance in public cloud can pull through Hyper-V adoption on-prem for easier cloud extension. Microsoft’s overall account relationships (enterprise agreements) can bundle in this solution. | Low cost (often free) and no vendor lock-in. Can be tailored to specific needs, and no punitive licensing – good for custom large-scale cloud (e.g., many public cloud IaaS providers use KVM under the hood). In container space, Kubernetes (open source) has become standard – VMware had to adapt via Tanzu. The open solutions avoid single-vendor dependency, which some organizations prefer post-Broadcom acquisition. |

| Weaknesses | Customer concern about price hikes and support under Broadcom – some fear innovation might lag or costs rise (Broadcom has significantly raised prices for bundled packages. Competition from public cloud: as more workloads shift to AWS/Azure, VMware must provide compelling hybrid value. Also VMware’s attempts in emerging areas (containers, modern apps) face stiff competition from cloud-native tools. | Hyper-V historically lags VMware in high-end features and scalability (e.g., VMware leads in supporting huge VMs, advanced VMotion capabilities, etc.). Azure Stack is relatively newer and less proven than VMware in on-prem deployments. Microsoft also directs a lot of focus to pure Azure, so on-prem tool development not always top priority. | Fragmented support – no single throat to choke for issues, which enterprises often require. Lacks unified management out of the box (though Red Hat provides some). Not as feature-rich (for example, live migration, storage management may not be as seamless). For companies without strong in-house IT engineering, open-source solutions can be complex to implement and maintain compared to VMware’s polished offerings. |

Table – Competitive Comparison: VMware (Broadcom) vs. Enterprise Virtualization Alternatives. VMware remains the leader in data center virtualization due to its rich features and installed base. Microsoft offers an integrated alternative especially attractive to Windows-centric shops, while open-source solutions appeal on cost and flexibility. Broadcom’s stewardship of VMware brings efficiency but has raised customer concerns about cost, which competitors may attempt to exploit.

Mainframe and Enterprise Software (CA Technologies)

Broadcom inherited a broad portfolio of mainframe software and enterprise DevOps tools from CA Technologies. This includes products that run on IBM Z mainframes – e.g. CA DB2 and IMS tools, CA SYSVIEW, CA 7 workload automation, mainframe security (ACF2, Top Secret), and many others that are essential for large enterprises running mainframes. It also includes enterprise software for distributed systems such as Clarity PPM (project portfolio management), DX AIOps (monitoring), application testing and development tools (e.g. CA Endevor for mainframe code management, Automic automation). These products are typically legacy but mission-critical applications in IT operations, used by banks, insurers, governments and others with mainframe or large-scale computing environments. Prior to VMware, CA was the bulk of Broadcom’s software segment revenue (~$6–7B/year). Under Broadcom, CA’s business has been run with an emphasis on profit and stability. Broadcom has continued to support and update these products for existing customers, while streamlining the business (e.g., rationalizing sales and marketing). The mainframe software market grows slowly (low single digits) but is very high margin. Broadcom’s CA division likely maintains strong cash flows as customers remain on maintenance contracts given the lack of alternatives (if you run an IBM mainframe, you likely use CA/Broadcom tools or IBM’s own tools).

– Market Performance & History: CA Technologies (formerly Computer Associates) had a long history as a consolidator of mainframe software companies. By the time Broadcom acquired CA in 2018, CA’s growth was low but it had extremely high recurring revenue from existing clients. Broadcom has largely met expectations of keeping that revenue stable. For example, Infrastructure software (pre-VMware) was roughly $6.6B in FY2020 and $7.07B in FY2021, reflecting slight growth, likely from renewing contracts with some price uplift and cross-selling. Broadcom likely invests just enough to keep the software updated for new IBM mainframe generations (e.g., ensuring compatibility with IBM’s z15, z16 systems). A key element is Broadcom often sells these as an integrated solution with the hardware connectivity business – for instance, bundling mainframe software tools with Brocade Fibre Channel networks or with security products. The historical development of these CA products is decades old; Broadcom itself has not needed to innovate heavily here, as the mainframe environment is stable. In enterprise (non-mainframe) software from CA, some tools (like Clarity PPM) still see use beyond mainframe shops and have competitors in the market, but Broadcom’s interest in aggressively developing them has been limited. Despite the stagnant nature, this segment is strategically important for Broadcom’s relationships with large enterprises – it gives Broadcom a foot in the door to sell additional solutions (e.g., security or VMware) to the same customers.

– Competitive Landscape: In the mainframe software arena, the primary competitor is IBM itself. IBM provides the mainframe hardware and also offers its own suite of software (for example, IBM has analogous products: Tivoli for management, RACF for security, Db2 tools, etc.). Many customers run a mix of CA(Broadcom) and IBM tools. Third-party competition is limited because this is a niche market – other players include BMC Software (which offers mainframe management tools and was a rival of CA for decades) and some smaller specialists. In Broadcom’s other enterprise software (like AIOps, PPM), competitors include vendors like Dynatrace, Splunk (for monitoring) or Planview, Microsoft Project (for PPM). But Broadcom’s strategy under Hock Tan is not to compete head-on in highly dynamic markets; instead it milks established franchises. Thus, Broadcom isn’t actively trying to beat Splunk or ServiceNow in AIOps, for example – it simply continues to serve existing CA customers who use CA’s DX Infrastructure Manager, etc. Table provides a high-level comparison focusing on mainframe solutions. Broadcom/CA’s advantages are the deep domain expertise and integration of their tools with enterprise workflows (many large IT shops have used CA products for 30+ years, building them into processes). Broadcom as a steward has given assurance of support, which for risk-averse mainframe clients is key. IBM’s advantage, of course, is that it owns the platform and can offer bundle deals (hardware, OS, and software together). BMC, now a private company, tries to compete by focusing solely on mainframe and cloud operations software, marketing itself as more agile and customer-focused than the larger vendors. Broadcom’s CA unit holds its ground largely due to customer lock-in and inertia – replacing core mainframe job schedulers or security systems is often not worth the risk for most enterprises, so they renew licenses with Broadcom indefinitely. This gives Broadcom pricing power, although it must be cautious not to push too hard (to avoid driving customers to IBM or others). In summary, Broadcom’s mainframe software segment is stable and oligopolistic, with Broadcom (via CA) and IBM sharing the pie, and little threat from new entrants.

| Mainframe Software & Enterprise Tools | Broadcom (CA) – Mainframe Tools | IBM Software – z Systems & Middleware | BMC Software – Mainframe & AIOps |

| Core Offerings | CA Broadcom offers: Mainframe performance monitors (e.g. SYSVIEW), job schedulers (CA 7), database management for Db2/IMS, security management (ACF2, Top Secret), and dev/test tools (Endevor, COBOL testing). Also enterprise management like Clarity PPM, Automation (Autosys) and AIOps (DX platform) for distributed systems. | IBM offers parallel products: OMEGAMON monitors, Tivoli Workload Scheduler, Db2 Tools, RACF security, etc., often bundled with the IBM z/OS operating system or sold as add-ons. IBM Middleware (CICS, IMS) and transaction monitors are part of its suite. Also provides modern devops for mainframe via UrbanCode and others. | BMC offers MainView monitors (compete with CA SYSVIEW), Control-M scheduler (a strong competitor to CA 7, also works cross-platform), security via BMC AMI (after acquiring Compuware’s security). BMC also has Helix and TrueSight for AIOps/monitoring across hybrid environments. Focuses on optimization and cost reduction for mainframe shops. |

| Customer Base | Most IBM mainframe clients globally; CA’s software historically had 1,500+ mainframe customers. Now these are Broadcom’s clients, who typically also use IBM software – many run a mix. CA’s distributed tools have a few thousand enterprise users as well (for PPM, etc.). | Essentially every mainframe user (IBM includes some tools with the platform). IBM’s software is often default for core functions (e.g., IBM’s RACF is embedded in z/OS for security, but some use CA’s ACF2 instead). IBM leverages hardware sales to cross-sell software. | Several hundred large mainframe customers – BMC is often the alternative supplier if not using CA/Broadcom. BMC’s Control-M is quite popular even beyond mainframe (workload automation for distributed systems too). BMC’s newer AIOps solutions target companies modernizing operations who might not want CA’s or IBM’s older tools. |

| Strengths | Legacy of trust and reliability – CA tools have been refined over decades for high-volume, mission-critical processing. Broadcom provides strong support and isn’t likely to discontinue products (reassuring for customers). Often, CA tools have unique features or customization that clients depend on. Broadcom can bundle software and semiconductors (e.g., discounts if customer also buys Brocade SAN gear). | Platform owner advantage – IBM’s tools often work at a lower level (some integrated into OS). Single-throat support for entire stack appeals to some CIOs. IBM invests in mainframe R&D continuously (new features for new hardware releases). Deep global services arm to support implementations. | Singular focus on IT operations software without hardware distractions. BMC has a reputation for slightly better customer service/flexibility than CA or IBM. Control-M, for example, is considered very user-friendly and is a market leader in job scheduling. BMC innovated in cost optimization (identifying mainframe cost savings) which appeals to customers under budget pressure. |

| Weaknesses | Limited growth/new innovation – mainly sustaining existing software. Broadcom’s model might raise maintenance costs over time (customers could resent this). Not a full platform provider (depends on IBM’s mainframe platform staying relevant). Some CA products on distributed side have fallen behind modern competitors (e.g., DevOps tools vs. Atlassian or Security vs. newer IdM platforms). | Often more expensive if taken à la carte; IBM’s bundling can sometimes force customers to take products they don’t use. Some IBM tools historically were less user-friendly (giving rise to CA/BMC alternatives in the first place). IBM’s focus is split between mainframe and many other businesses, so niche tool enhancement can lag (unless tied to hardware sales). | BMC is much smaller than Broadcom or IBM, so it lacks the sheer resources – for instance, it can’t bundle with hardware sales or offer the same breadth (it doesn’t have a database product, for example). Some customers worry about BMC’s long-term stability (as a private, PE-owned firm). It must continually prove its tools are as good or better to dislodge incumbent CA/IBM deployments. |

Table – Competitive Comparison: Broadcom (CA) vs. Competitors in Mainframe/Enterprise Software. Broadcom’s CA unit and IBM largely share the mainframe software market, with BMC as a notable third-party competitor in certain tools. The competition is characterized by an emphasis on reliability and long-term support rather than rapid innovation, given the critical nature of mainframe systems.

Enterprise Security (Symantec)

Broadcom acquired Symantec’s Enterprise Security business in late 2019. This brought a suite of security software including endpoint protection (Symantec Endpoint Security, a leading antivirus/EDR solution for businesses), network security (Secure Web Gateway, ProxySG), Data Loss Prevention (DLP), and identity/access management (Symantec VIP). These tools are used by corporations to secure endpoints (PCs, servers), filter web traffic, prevent data breaches, and authenticate users. Under Broadcom, the Symantec enterprise division has been run similarly to CA – focusing on top customers, cutting costs, and integrating the products into bundles for large enterprises. Symantec’s consumer business (NortonLifeLock) was not part of Broadcom’s purchase, so Broadcom strictly sells to enterprises. The revenue of this unit is not broken out publicly post-VMware, but before VMware, Symantec contributed on the order of ~$2B/year (Symantec was ~$2.5B annual enterprise rev at acquisition, likely modestly lower now after Broadcom’s adjustments).

– Product Performance & Development: Symantec’s products were once market leaders (e.g., Symantec Endpoint Protection (SEP) had significant market share in corporate AV). However, the cybersecurity market is fast-moving, and Symantec (pre-Broadcom) was facing stiff competition from newer players like CrowdStrike (in endpoints) and Zscaler (in secure web gateways). Broadcom’s approach after acquisition was to streamline and maintain: it reduced investment in broad sales of Symantec products and instead focused on selling to existing large installed base customers, ensuring renewals. Some innovation continues (Symantec releases updates to its endpoint agent and cloud security platform), but Broadcom has not been seen as aggressively expanding this portfolio. Despite that, the Symantec suite covers a broad range of security needs and can be appealing to companies that prefer a single vendor for multiple security layers. Broadcom has likely bundled endpoint, DLP, and network security together for discounts to retain customers. Symantec’s historical strength was its comprehensive coverage and threat research; those remain, but in the last couple of years Symantec’s mindshare has slipped as pure-play security firms grab headlines. Even so, many large enterprises and government agencies still rely on Symantec solutions for critical protection – these customers often value stability and integration (which Broadcom provides) over having the absolute bleeding-edge tech.

– Competitive Landscape: In enterprise security software, competition is intense. For endpoint security, competitors include CrowdStrike, Microsoft (Defender for Endpoint), Trellix (McAfee), Trend Micro, among others. In network security and web proxy, key competitors are Zscaler, Cisco (Umbrella), Palo Alto Networks (Prisma Access). In DLP, competitors include Forcepoint, Microsoft, McAfee. Broadcom/Symantec’s competitive advantage is offering an integrated security portfolio from a single vendor – some peers have point solutions (e.g., CrowdStrike does endpoint, Zscaler does cloud proxy, etc.). Broadcom can pitch a unified cyber defense platform (Symantec Enterprise Cloud) covering endpoint, network, email, DLP, identity. However, many buyers now favor best-of-breed and cloud-delivered security, where newer vendors excel. Table compares Symantec (Broadcom) with a couple of significant competitors. Symantec still ranks among leaders in independent evaluations (for example, Symantec Endpoint typically scores high in AV tests, and its DLP is often top-ranked). Broadcom’s massive scale and support organization can be a plus for global customers. A disadvantage for Broadcom is the perception that it is not as focused on innovation in security as specialized firms – indeed, after the acquisition, some Symantec talent and customers left, concerned that Broadcom would put the products in “harvest” mode. Broadcom has attempted to assure customers by continuing threat research (Symantec’s Threat Hunter team is still active) and releasing new features (like Zero Trust Network Access capabilities). Still, market momentum in enterprise security has shifted to cloud-native providers and next-gen startups. Broadcom seems content to retain the large installed base and ensure they renew maintenance/subscriptions, rather than win every new deal. The Symantec business remains highly profitable, contributing significantly to Broadcom’s software margins (achieved ~>50% EBITDA margins post-integration).

| Enterprise Security Software | Symantec Enterprise (Broadcom) | CrowdStrike (Next-gen Endpoint) | Zscaler (Cloud Security) |

| Primary Domains | Broad portfolio: Endpoint Protection (antivirus/EDR), Email Security, Web Security (ProxySG, Secure Web Gateway), Data Loss Prevention, Identity (VIP), Endpoint Management (Altiris). Solutions can be on-prem or cloud-managed (Symantec Enterprise Cloud platform). | Focused portfolio: Cloud-delivered Endpoint Detection & Response (EDR) and extended detection (XDR) via its Falcon platform. Also offers cloud workload protection. Known for AI-driven threat detection on endpoints. | Focused portfolio: Secure Web Gateway, Cloud Access Security Broker (CASB), Zero Trust Network Access – all via its cloud platform (SASE model). Provides safe internet access and internal app access from the cloud, replacing traditional on-prem proxies/VPNs. |

| Target Customers | Large enterprises and governments that need a full suite of security controls, often those with complex legacy infrastructure (on-prem data centers, offices, remote users). Many have long-used Symantec and value continuity. | Enterprises of all sizes, especially those seeking cutting-edge endpoint protection with strong cloud management – often companies moving away from legacy AV (Symantec/McAfee) to more proactive threat hunting. | Enterprises embracing cloud-first IT, remote work, and looking to eliminate on-prem security appliances. Often mid-to-large organizations seeking simplified management and scalability through a cloud security service. |